If you’re facing financial difficulties and worried about losing your home, understanding the house repossession process in the UK is important.

House repossession is a legal process. It happens when a lender takes back a property because of missed mortgage payments. This is often a last resort for both the lender and the homeowner. Knowing how long this process takes can help you take the right steps and check alternatives before it’s too late.

Repossession is typically a last resort after multiple warnings and legal proceedings. It’s important to note that it doesn’t happen overnight—there are various steps in the process, including lender notifications, court involvement, and opportunities for the homeowner to negotiate or settle the debt before eviction.

For many, repossession is not just about losing a house—it’s about losing financial stability, security, and a place to call home. However, knowing the process can help homeowners take action before it reaches that stage.

What Are Mortgage Arrears?

Mortgage arrears occur when you miss one or more mortgage payments. Falling behind on payments puts you at risk of repossession, but it doesn’t happen overnight. Lenders are required to follow a set process, giving you a chance to resolve the situation.

How many months mortgage arrears before repossession?

You might be stressing about “how many missed mortgage payments before repossession?”. In most cases, lenders will think about repossession after 3 to 6 months of missed payments. However, this can change based on your lender’s rules and if you are working with them to fix the problem. Most mortgage lenders will try and help you get into a better financial situation before declaring a late payment.

Reasons for House Repossession and Its Effects

When mortgage payments are not made for a long time, usually many months, the house is repossessed. Financial hardship brought on by a loss of employment, a reduction in income, or unforeseen expenses are common causes; rising interest rates that make monthly repayments unaffordable; significant life events that impact financial stability, such as divorce, illness, or bereavement; and poor money management that results in unmanageable debt or excessive spending.

Although repossession mostly affects homeowners, its impacts are not limited to them. While landlords who have buy-to-let mortgages run the risk of losing their houses if they don’t make loan payments, families may be evicted and find it difficult to find other housing. Furthermore, repossessed houses sometimes sell for a discount, which could affect the value of nearby real estate.If you’re wondering what happens to bank repossessed houses, it’s worth noting that these properties sometimes sell for a discount, which could affect the value of nearby real estate.

Financial Hardship and Job Loss

Losing a job or experiencing a significant drop in income is one of the leading causes of mortgage arrears. Without a steady income, covering essential expenses—including mortgage payments—becomes increasingly difficult. Even if a homeowner secures new employment, catching up on missed payments can be challenging, especially if legal proceedings have already begun. While some lenders offer temporary relief, such as mortgage holidays, repossession remains a risk without a long-term financial solution.

Unexpected Life Events (Illness, Divorce, Bereavement)

Major life events can significantly impact financial stability.

- Divorce or separation: When couples split, one party may struggle to afford the mortgage alone. If an agreement isn’t reached, the lender may intervene.

- Serious illness or disability: Health issues can prevent homeowners from working, leading to reduced income and difficulty keeping up with payments.

- Bereavement: The loss of a spouse or co-borrower can leave the surviving homeowner unable to manage mortgage repayments on a single income.

Rising Mortgage Rates and Affordability Issues

Many UK homeowners have variable-rate or tracker mortgages, meaning their payments fluctuate with interest rate changes. When rates rise, monthly mortgage costs can increase significantly, making them unaffordable for some borrowers. Those who were previously managing comfortably may suddenly find themselves struggling, leading to missed payments and, ultimately, repossession.

Poor Financial Management or Unsustainable Mortgages

In some cases, repossession occurs due to poor financial planning or risky mortgage agreements. Common issues include:

- Overborrowing – Taking out a mortgage that is too large relative to income.

- High-interest subprime loans – Borrowing from lenders with steep rates that become unaffordable over time.

- Lack of financial cushion – Failing to budget for emergencies or unexpected costs.

Homeowners with interest-only mortgages may also face difficulties when their loan term ends, as they must repay the full amount. Without a repayment plan in place, lenders may have no option but to repossess the property.

Factors that influence the duration of mortgage arrears before repossession

- Lender’s Policy: Some lenders may act faster than others depending on their policies.

- Your Engagement: If you take action, talk to your lender, and set up a payment plan, you can delay or avoid repossession.

- Current Market Conditions: Economic factors can influence lenders’ actions regarding repossession. For example, a recession or a cost-of-living crisis may make lenders less aggressive.

The House Repossession Process in the UK

Step 1: Initial Steps by Lender

When you miss a payment, the lender will first notify you of the missed instalment. After a few missed payments, they will send a more formal demand. At this stage, lenders must provide you with information about your rights and the possible outcomes, including repossession.

Missed Payments & Lender Warnings

-

- After several missed mortgage payments, the lender issues formal warnings and may offer repayment options.

- Some lenders provide mortgage payment holidays or restructuring plans to help borrowers get back on track.

- Homeowners can also seek independent financial advice to explore alternatives.

Step 2: Legal Proceedings

If no payment agreement is reached, the lender may start legal proceedings. They will apply to the court for a repossession order, which can take several weeks to process. You’ll receive notice of the court hearing, where you have the opportunity to attend and defend yourself. If the court rules in favour of the lender, a repossession order will be granted.

Court Action & Possession Order

-

- If no resolution is reached, the lender can apply for a Possession Order from the court, allowing them to take control of the property.

- Homeowners have the right to challenge the order in court and may request additional time to sell the property themselves.

- If the court rules in favour of the lender, a date for repossession will be set. In some cases, homeowners can still negotiate a sale before eviction occurs.

Step 3: Timeline of the Repossession Process

Once the court order is issued, the timeline for actual repossession depends on the type of order:

- Suspended Possession Order: If you agree to catch up on payments, repossession can be suspended, delaying or halting the process.

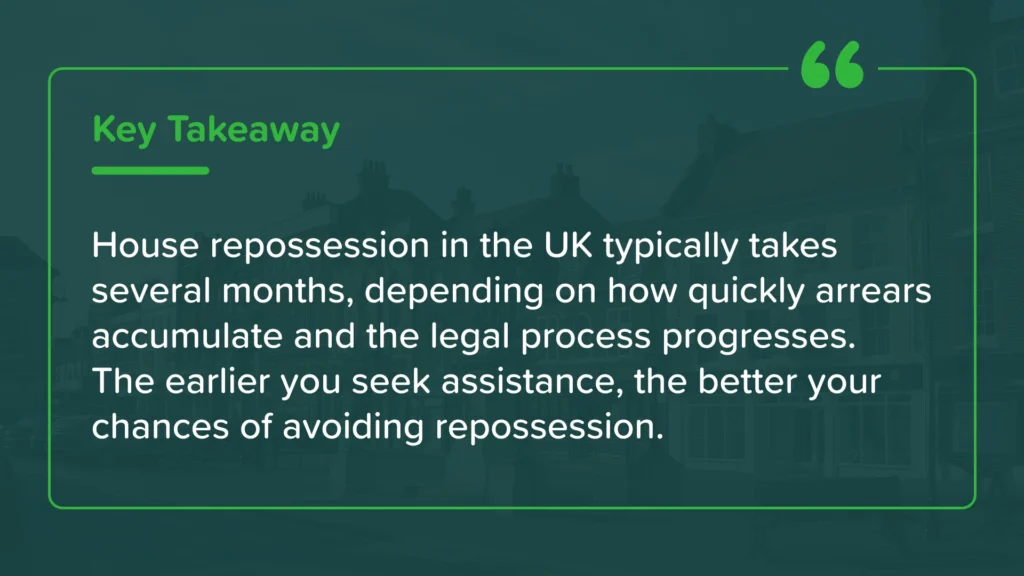

- Outright Possession Order: This usually gives you 28 days to vacate the property. In total, from the first missed payment to repossession, the process can take anywhere from 5-12 months, depending on individual circumstances and court availability.

Eviction Notice

-

- If the court grants the order, the homeowner is given a deadline to vacate. Bailiffs may be involved if they refuse to leave.

- At this stage, seeking professional help from property specialists or solicitors is crucial.

- Some homeowners may qualify for government support schemes to avoid homelessness post-eviction.

Step 4: Lender Secures the Property

Once the property becomes vacant, the lender takes immediate steps to secure it by changing the locks and ensuring it is in a saleable condition. Basic maintenance or minor repairs may be carried out to enhance its appeal, making it more attractive to potential buyers. Additionally, security measures such as boarding up windows or installing surveillance may be implemented to prevent vandalism, theft, or unauthorised occupancy.

Step 5: House Put Up for Sale

After securing the property, the lender lists it for sale, often pricing it competitively to ensure a quick sale and recover the outstanding debt. In many cases, properties are sold below market value to attract investors or first-time buyers looking for a good deal. The goal is to expedite the selling process while maximising returns. Find out how our cash house buying company can help you

Overview of the UK Laws Governing Repossession

In the UK, repossession is regulated by several legal frameworks designed to ensure fair treatment for homeowners. Key laws include:

- The Mortgage Conduct of Business (MCOB) Rules – Set by the Financial Conduct Authority (FCA), requiring lenders to treat borrowers fairly and offer alternative solutions before repossession.

- The Administration of Justice Act 1970 & 1973 – Provides legal protections, allowing courts to delay repossession if borrowers can prove they can repay arrears within a reasonable timeframe.

- The Housing Act 1988 & 1996 – Covers repossession for rental properties, protecting tenants if a landlord’s property is repossessed.

Understanding these legal protections is crucial for homeowners facing repossession, as they may have options to negotiate or delay the process.

Costs Associated with House Repossession

Repossession is not just emotionally draining; it’s financially costly as well.

Financial implications for homeowners

For homeowners, charges like legal fees, court costs, and interest on missed payments can quickly add up. Depending on your lender, the total cost of repossession can range from hundreds to thousands of pounds.

The financial impact is also beyond losing your home. Repossession damages your credit score, making it difficult to obtain credit in the future. The property might be sold for less than you expected. If the sale price doesn’t cover the full mortgage, you could still owe the lender.

Additional Costs for Lenders

Lenders also incur costs during repossession. They must cover legal fees, property maintenance, and the expense of selling the home. These costs are often passed on to the homeowner, worsening the financial burden.

How to Stop House Repossession

Facing repossession is scary, but there are options. Here’s what you can do:

- Seek Help Early: Contact your lender as soon as you know you’ll miss a payment. They may be able to offer tailored solutions.

- Consider Selling Quickly: If selling your house is the best option, Zapperty can help! We offer a fast, hassle-free way to sell your property and avoid repossession altogether.

Avoid House Repossession—Sell Your House Quickly. Don’t wait until it’s too late. If you’re struggling to keep up with mortgage payments, selling your home quickly might be the best option. At Zapperty, we give cash offers within 60 minutes. We can finish the sale in just 7 days. This helps you stop house repossession and move on with peace of mind.

FAQs

How long does it take to repossess a house in the UK?

The repossession process typically takes 5-12 months from the first missed payment to when you have to leave the property. The timeline can be shorter if the lender moves quickly, or longer if you work out a repayment plan.

How much does it cost to repossess a house?

For homeowners, repossession can cost thousands of pounds, including legal fees, court costs, and interest on missed payments. The financial damage doesn’t stop there—repossession negatively impacts your credit score.

Can I stop repossession after receiving a court order?

It’s possible, but it’s more challenging. You may need to seek legal advice and explore options like bankruptcy or negotiating a payment plan.

What happens to my belongings if my house is repossessed?

You may have limited time to remove your personal belongings before the lender takes possession of the property. It’s advisable to consult with legal professionals to understand your rights in this situation.

Is selling my house the only way to avoid repossession?

While it is often the best solution, there may be other options. You could negotiate a payment plan or seek debt relief. However, selling your house can provide a more immediate resolution.

Can I sell my house myself if I’m facing repossession?

Yes, you can. However, the process can be time-consuming and stressful, especially if you’re already dealing with the threat of repossession. Consider using a service like Zapperty to speed up the sale.

How long does it take to sell a house if I’m facing repossession?

The speed of the sale can vary depending on market conditions and the urgency of your situation. A service like Zapperty can often facilitate a faster sale compared to traditional methods.

What happens to the remaining debt after my house is repossessed?

The lender may still pursue you for the remaining debt, even after the property is sold. This could involve legal action or garnishing your wages.

Can I get my house back after it’s been repossessed?

In some cases, you may be able to buy back the property. However, this is usually a complicated process and needs certain conditions.

How long will it be before I can buy another house after repossession?

You might have to wait before you can get a new mortgage. This is especially true if you have a recent repossession on your credit report. The length of the waiting period can vary depending on your credit history and the lender’s requirements.